Paper invoices: When are they acceptable, and when do they pose a risk?

E-Invoice

Paper Invoices: When Are They Still Acceptable, and When Do They Pose a Risk? | Syneo

When is it still acceptable for a company to use paper invoices, and when does this pose a business, audit, or compliance risk? A quick guide to risks and minimum controls.

paper-based invoices, e-invoices, digitization, audit, archiving, NAV, compliance, automation, ERP, data quality

March 25, 2026

By 2026, paper-based invoicing will still be used by many companies simply out of “habit,” but it will pose a growing business and compliance risk in an increasing number of cases. Not because every paper invoice will suddenly become illegal tomorrow, but because the environment is changing rapidly: the Hungarian Tax and Customs Administration’s (NAV) online data reporting requirements, EU standardization (such as EN 16931), the digitization of supply chains, and the need for auditability together could create a situation where paper is already expensive, slow, and difficult to secure.

The following guide will help you determine when paper-based processes can remain in place and when they become particularly risky, as well as what “minimum” controls can be implemented to reduce exposure while you transition.

First, let’s clarify: what counts as a paper invoice, and what doesn’t?

In practice, there are three situations that are often confused:

Paper invoice: You physically issue (print) it, physically hand it over or mail it, and keep a paper copy.

A printed electronic invoice: the invoice was originally in electronic form (such as PDF or a structured format), but someone prints it out during the process “because it’s more convenient.” This does not automatically simplify issues related to its legal status, retention, and admissibility as evidence.

Digitized paper (scanning): It arrives on paper, then you scan it, and the accounting/ERP system processes it digitally. This is better than using paper exclusively, but scanning alone does not magically turn the document into an “e-invoice.”

A significant portion of the risks stems from the fact that companies expect paper-based discipline in a digital audit environment, or conversely, want digital convenience with paper-based controls.

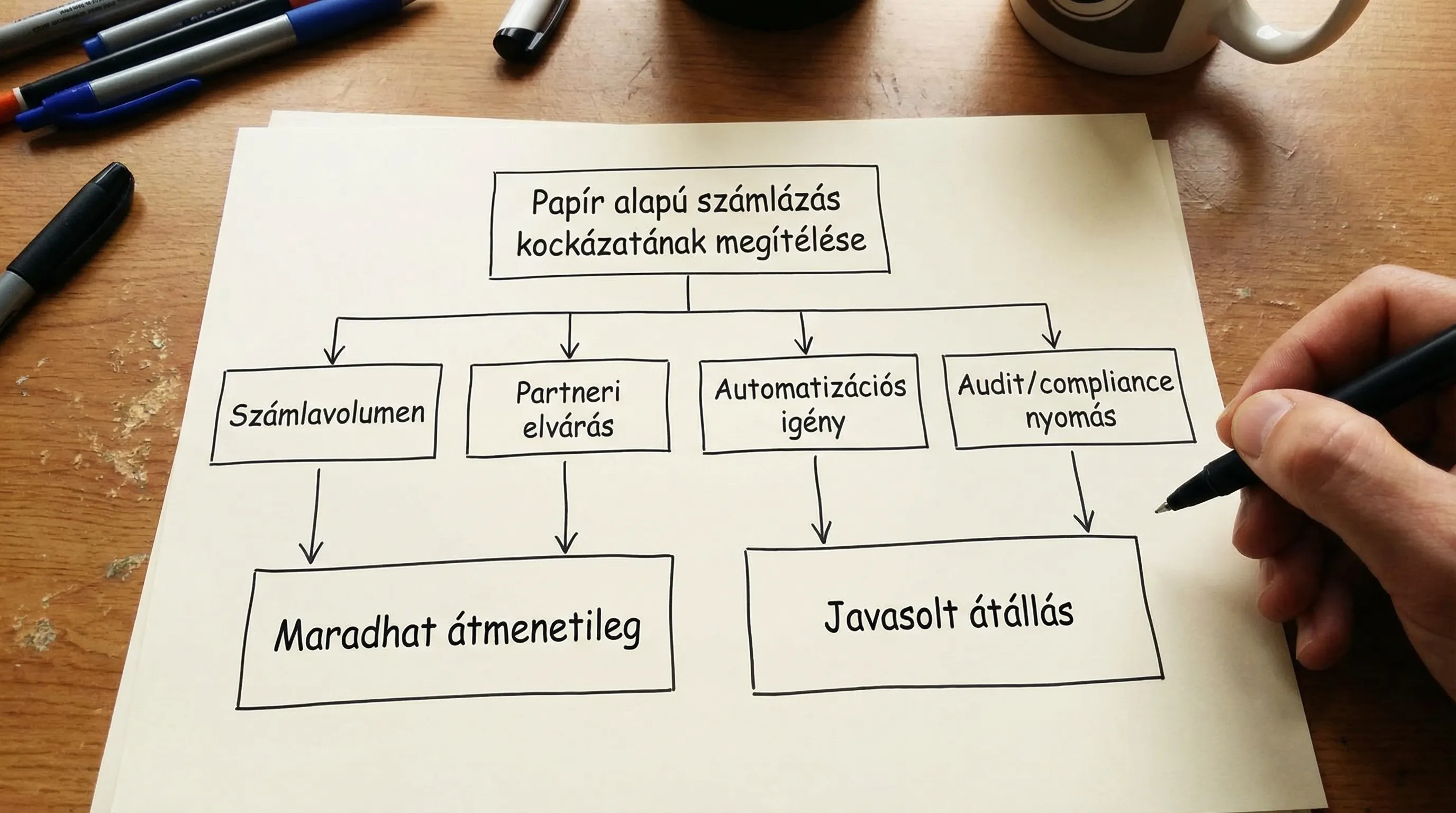

When can paper invoices realistically still be used in a corporate setting?

Paper generally remains viable when volumes are low, automation requirements are minimal, and partners are willing to accept it.

Typical situations where paper is still used by many companies (including for business purposes):

Very low invoice volume: just a few incoming and outgoing invoices per month, with minimal exception handling.

Simple, with few system integrations: no ERP or only a minimal financial module, and no automated approval workflow.

A group of partners that specifically requests paper (e.g., legacy processes, limited digital maturity). It is important to note here as well: a “request” is not the same as a “contractual, auditable agreement.”

As a contingency plan: in the event of a failure in the billing or delivery system, a temporary, controlled solution is required.

However, what is true in almost all cases today is that even when using paper invoices, the issuance may still be subject to the NAV Online Invoice data reporting requirement, and the risk of errors, delays, and data quality issues is typically higher than with paper invoices. The details always depend on the specific transaction and parties involved, so it is advisable to follow the official NAV guidelines (such as the NAV Online Invoice interface and documentation).

When Are Paper Invoices Risky? The 6 Most Common Risks

Paper isn't just "slower"; in certain situations, it's also hard to defend. It's the following patterns that really cause problems.

1) The volume increases, and error handling is triggered

The more invoices we receive, the more:

typo, missing data, incorrect tax ID number

duplication

item awaiting approval

disputed performance

On paper, these details typically get "scattered" across emails and Post-it notes, making it difficult to explain during an audit why things happened the way they did.

2) The inflow of funds is slowing down, and cash flow is deteriorating

It is more common with paper that:

The bill will arrive later

will be recorded later

The follow-up around the payment deadline will take place later

If delivery is uncertain for outgoing invoices, this can lead to disputes and delays (especially with larger B2B partners).

3) There is a higher risk of data quality and accounting errors

Errors in manual data entry and data capture from scanned documents (OCR) directly affect:

VAT handling

general ledger posting

partner master data

reconciliations (bank statements, supplier statements)

If the goal is to increase the proportion of “touchless” (contactless) accounting, paper is generally the most expensive factor. These cost differences are regularly highlighted in international e-invoicing industry reports (such as the Billentis e-invoicing reports ).

4) It is more difficult to provide auditable evidence (authenticity, integrity, legibility)

Within the EU VAT framework, the principles of authenticity, integrity, and legibility are key requirements for invoices, which can typically be reinforced through process controls, audit trails, or appropriate electronic solutions (see, for example, the framework of EU VAT Directive 2006/112/EC ).

You can set up disciplined controls on paper, but this is often more expensive than doing it well digitally.

5) Archiving and retrieval risk

Retention periods and traceability are not just about “files on a shelf.” In a typical audit, what matters is:

Can the document be found quickly?

Is the version and "original" status clear?

Can it be proven who accessed it and when?

If there is no strong link between the paper-based records and the digital accounting system, it becomes difficult to provide evidence.

6) Information security and data protection risks

Incidents that are common in paper-based systems are easier to control in digital systems:

unauthorized access (documents left on the desk)

lost envelope, incorrect address

too broad access (everyone can see everything)

If you’re already facing increasing compliance pressures (such as supplier audits, ISO, or NIS 2 requirements), paper documents are often the weak link.

Quick decision matrix: stick with paper, or is it time to switch?

The table below is a quick "situation assessment" framework for executives. It is not a legal opinion, but rather a risk filter.

Situation | Business risks associated with paper | What should you do? |

1–20 invoices per month, few partners, minimal exceptions | Low-medium | It can stay for now, but set up basic controls (see below). |

20–200 invoices per month, multiple locations, or multiple approvers | Medium-high | Hybrid model: digitization of outgoing invoices, workflow for processing incoming invoices. |

Over 200 invoices per month, ERP, multiple systems, integration needs | High | Structured e-invoicing and automated processing, with ERP integration. |

Large corporate partners, public procurement, international supply chain | High | EN 16931 compliance; testing of standard channels (e.g., EDI/PEPPOL). |

Lots of disputes, lots of credit notes, lots of adjustment invoices | High | Strengthening the audit trail and digitizing delivery and status management. |

Audit, compliance, security-critical | High | Roles, logging, access management, and archiving. |

If there’s still paper left: the “minimum” controls worth implementing

If there are business reasons for keeping records on paper for a while, it’s still worth treating this as a structured process rather than a secondary administrative task.

The greatest gains usually come from consistency, not from expensive equipment.

Clear rules regarding "originals": what counts as an original, where it is located, and who manages it.

Centralized filing and unique identifier: the document and the accounting entry must be linked.

Standard scanning: uniform resolution, file naming convention, required metadata (partner, date, amount, status).

Approval workflow: at least one digital approval trail (who approved what and when).

Access management: Key management for paper archives and permissions for digital folders should be auditable.

Archiving policy: retrievability and consistent backup procedures for scanned files.

If you are interested in the minimum security and access management requirements for e-invoices, here is some useful related material:

"True" risk reduction: a gradual transition, not a one-time major project

Many people mess up the digitization of invoicing by trying to do everything at once: a new invoicing system, a new ERP workflow, a new archiving system, and new integrations. Instead, a gradual, measurable transition typically works better in 2026.

1) Stabilizing outgoing invoicing (delivery and status)

The quickest way to make a profit is often to simply:

reaches the partner more quickly

delivered with proof of receipt

also available in a machine-readable format

Detailed, beginner-friendly steps for implementing e-invoicing can be found here:

2) Invoice processing: workflow + exception handling

On the landing page, the goal is usually:

shorter lead time

less manual recording

fewer duplicates and errors

In many cases, the question isn’t whether “OCR is needed,” but rather how exceptions (incorrect data, missing purchase orders, disputed items) will be handled. A helpful overview of accounting automation:

3) Integration with ERP and auditable archiving

Scaling depends on the following:

What is the quality of the data model and the master data?

how invoice data is routed to the appropriate system (ERP, accounting, BI)

What evidence is available in the event of an audit?

You can find a comprehensive overview of the regulatory and technical trends in the e-invoicing landscape for 2026 here:

Paper vs. Digital: A Management Comparison (Not Marketing, but Decision Support)

The table below helps you quickly see where the differences lie in day-to-day operations.

Consideration | Paper invoice | Electronic invoice (well-designed) |

Lead time | Slower (delivery, recording, approval) | Shorter, automatable statuses |

Error rate | Higher (manual recording, readability, duplication) | Lower (validation, structured data) |

Auditability | It's difficult; there's a lot of "manual verification" | Stronger audit trail, logging |

Archiving, retrieval | Physical storage, slow retrieval | Searchable, can be protected with permissions |

Integration with ERP | Limited, many manual steps | API, EDI, imports, standard formats |

Safety | Physical access and the risk of loss | IAM, RBAC, MFA, and logging can be integrated |

How can Syneo help if you switch from paper to digital?

Digitizing invoicing is typically not just about “choosing an invoicing software,” but involves processes, integration, and security as well. In such projects, Syneo generally adds value in the following ways:

Identification of requirements and risks (process, compliance, audit)

system integration (billing, tax authority data reporting, ERP, DMS)

Implementation of controls and access management

A phased pilot approach with measurable KPIs

If the question now is, “Can we keep using paper, or is it already causing problems?”, it’s a good idea to start with a brief assessment of the situation and then decide on the minimum necessary steps. For more articles and an overview of our services, visit the Syneo website.