E-Invoice Rules 2026: Issuance, Submission, and Retention

E-Invoice

E-Invoice Regulations 2026: Issuance, Submission, and Retention | Syneo

2026 Practical Guide to Issuing e-Invoices, Submitting Them to the Tax Authority, and Long-Term Retention. Audit-ready processes, archiving controls, and compliance guidelines for businesses.

e-invoice, NAV Online Invoice, archiving, retention, compliance, EN16931, ERP integration, data protection, digital signature

April 18, 2026

By 2026, e-invoicing will no longer be a “convenience feature,” but rather a matter of compliance and operational efficiency: issuance, data reporting (submission) to the National Tax and Customs Administration (NAV), and long-term retention will be consolidated into a single, auditable process. Most errors do not stem from the content of the invoice itself, but from the surrounding controls: authorizations, logging, provable delivery, archive retrievability, and the management of NAV statuses.

This article provides a practical "2026 minimum guide": what a company needs to know about e-invoice regulations throughout the entire lifecycle of issuance, submission, and retention. (This does not constitute legal or tax advice; consult an accountant or tax advisor for specific cases.)

What will be considered an e-invoice in 2026?

Under Hungarian and EU regulations, the essence of e-invoicing is not that “we send it as a PDF,” but rather that the invoice is issued and received in electronic form, and that the following are ensured during storage:

authenticity of the document (who issued it),

data integrity (unchanged),

readability (understandable to humans).

In practice, these requirements can be met through a variety of technical solutions: controlled business processes, EDI/PEPPOL channels, digital signatures and time stamps, or a combination of these.

The trend for 2025 and 2026 is increasingly moving toward structured e-invoices (EN 16931 standard, machine-readable data content). If your company wants to automate accounting and invoice processing, the practical benefits of structured formats will be far more important in 2026 than the “paper vs. PDF” debate itself.

Reliable primary sources:

The EU Framework for Trust Services: the eIDAS Regulation

European Data Model for E-Invoices: An Overview of EN 16931

NAV Data Reporting and Technical Specifications: NAV Online Invoice

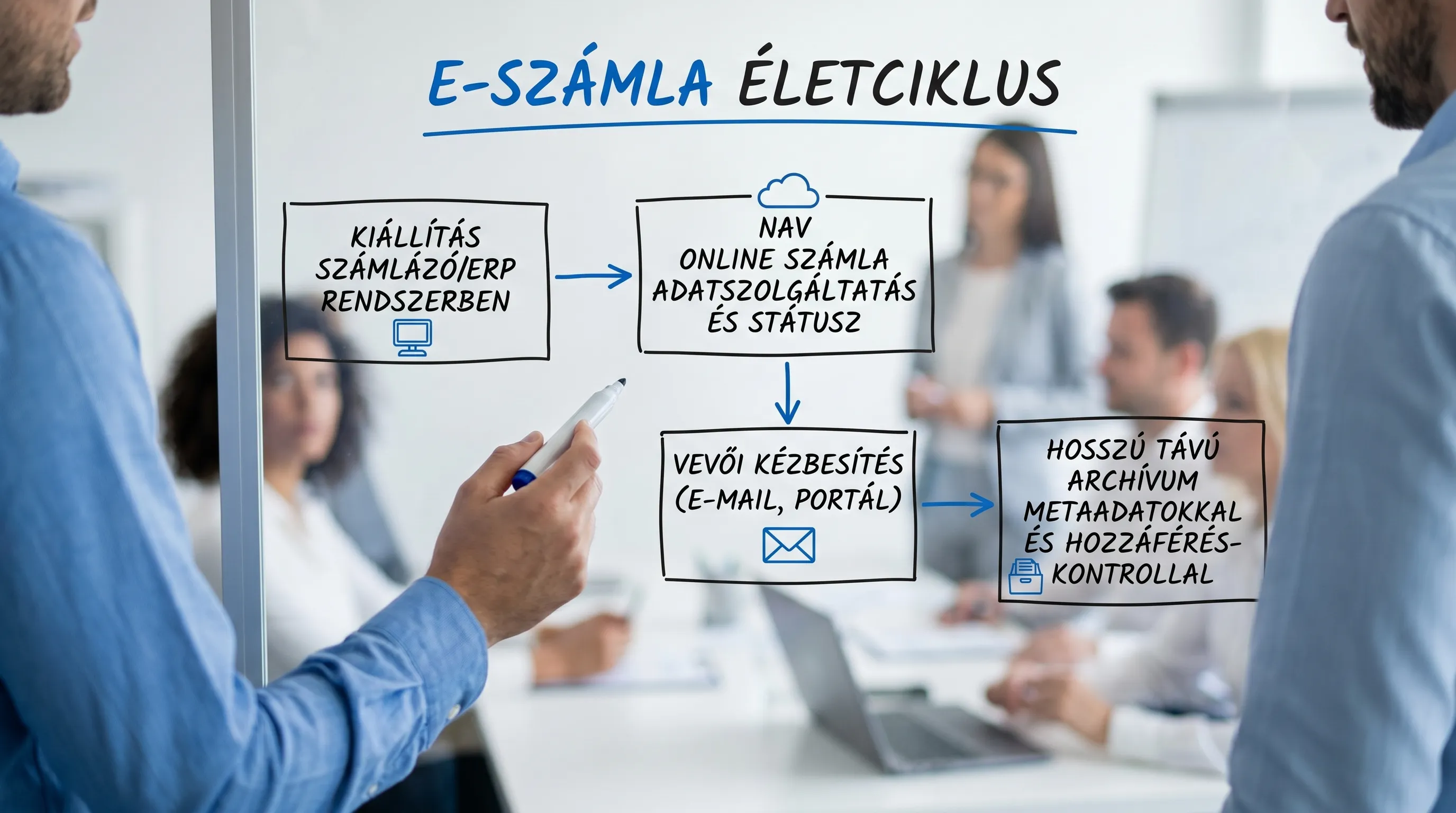

1) Issuance: the “correct” generation of an e-invoice

The exhibition requires addressing two dimensions simultaneously:

accounting/tax-related content (required data fields, accurate buyer-seller information, line items, VAT logic),

verifiable electronic record (how do you later prove that the invoice was authentic and unaltered)?

Mandatory principle: the auditable trail

By 2026, “audit trail” will be more than just a corporate buzzword. With a good e-invoicing process, you’ll always be able to answer:

who created the invoice,

when,

from which source data (order, delivery confirmation, contract),

what approvals have been granted,

what was sent to the customer,

what was reported to the NAV,

what was archived.

Format and production: what should be established as a rule?

The greatest operational risk is the “semi-electronic” state: multiple formats and delivery channels at the same time, and no standardized set of supporting documents.

It is a good idea to establish the following as an internal rule:

What types of invoices qualify as e-invoices?

in what format (structured XML and/or human-readable representation),

Through which channel do you deliver,

where the "golden copy" to be preserved is created.

If your team is wondering whether "digital signatures will be required" in 2026, you can find specific decision-making criteria here: Digital signatures for electronic invoices: Will they be required in 2026?

Customer Acceptance and Declaration: Don’t Just “Approve” It via Email

Many audit risks arise because the following issues have not been clarified: under what conditions the customer accepts the e-invoice, in what format, through what channel, and what constitutes delivery.

Practical example and requirements: E-invoice declaration: What should it include to be audit-compliant?

2) Submission / Data Reporting: NAV Online Invoice 2026 Minimum Requirements

For most companies, “submission” refers to the data reporting via NAV Online Invoice. By 2026, it will no longer be enough simply to submit the data successfully; the system must also operate reliably, measurably, and verifiably.

The 3 typical error levels in the NAV connection

In practice, errors typically fall into three categories:

data error (master data, tax ID, address, item logic, VAT relationships),

format / validation (schema, required fields, characters),

integration / operation (intermittent outages, excessive requests, keys, permissions, lack of retry mechanisms).

If you want to quickly triage and resolve NAV errors, this article is specifically designed with a "quick fixes" approach in mind: NAV e-invoicing: common errors and quick fixes for businesses

Minimum operating requirements: What does your system need to know?

In 2026, it is advisable to view NAV data reporting as a production integration process (rather than simply an “export button”). Minimum requirements:

Status management: Each invoice should be assigned a clear NAV status (submitted, accepted, rejected, being retried).

Idempotence and retry/backoff: Do not resend the request, but handle network errors.

Logging: Maintain a searchable request-response log (with appropriate data masking).

monitoring: keep an eye on the rejection rate to see if it rises.

This is typically where access rights and technical user accounts (keys) are configured: NAV e-invoice login: permissions, roles, error codes

3) Retention: archiving e-invoices in a way that ensures they remain accessible even after 6–8 years

The purpose of preservation is not simply to “store it somewhere,” but to ensure that it can be verified even years later:

This was the original invoice,

has not changed,

can be retrieved and read,

access rights are regulated,

the system's operation is documented.

In Hungarian practice, invoices are typically retained for several years (often for eight years), which means that technological changes (such as changes in file formats or system upgrades) also pose a real risk to the archive.

What constitutes the "evidence package" for a properly archived e-invoice?

When it comes to archiving, it’s best to think in terms of a package rather than a single file. Typical components:

the original electronic file of the invoice (structured and/or human-readable representation),

metadata (issuer, date, serial number, partner identifiers),

evidence related to delivery (when, via what channel),

NAV status and responses (reasons for acceptance/rejection),

proof of integrity (process control, hash, digital signature/timestamp, or other auditable method).

Archiving controls: what an auditor will typically ask for

The table below helps you align the requirements with what you should actually have "under control" by 2026.

Area | Requirement (in business language) | Practical evidence / control |

Innocence | Changes should not be made without being noticed | WORM-style storage or strong versioning, hashing/signing, audit log |

Traceability | It will be ready in 1–2 minutes, if requested | Indexed metadata, unique serial numbers and partner keys, search rules |

Access | Only authorized users can view and export | RBAC, MFA, separation of administrative duties, regular review of permissions |

Continuity | It remains protected even if the system is replaced | Migration plan, spot check, rollback test |

Privacy Policy | No leakage of PII or trade secrets | Encryption, masked logos, and DPIA where necessary |

If you're looking for a comprehensive, step-by-step checklist, you might want to read this: E-invoice 2026: Checklist for Issuance and Archiving

The "3-point" approach works when there is governance in place

In many organizations, e-invoicing “floats” somewhere between finance and IT. By 2026, this will typically pose a risk: if no one is assigned responsibility, errors will remain undetected for weeks.

Recommended minimum roles (not necessarily separate people, but assign names):

Business owner (finance/accounting): account details, processes, partner rules.

IT owner: NAV integration, logging, access, operations.

Compliance/internal controls: sample-based audits, evidence, audit support.

Related security requirements for e-invoicing environments: E-invoicing access: access management and security requirements

Quick Self-Assessment for 2026: Where Do Most Companies Fall Short?

The following points are typically “hidden” risks that only come to light during an audit or when the National Tax and Customs Administration (NAV) identifies a series of errors:

There is no standard rule regarding where the "original" invoice is located (in the ERP system? In an email? In the DMS?)

NAV rejections are handled manually; there is no verification or feedback regarding the master data

The archive cannot reliably verify its integrity (it contains only a folder with files)

Administrator privileges are too broad; there is no separate technical user management

There are no regular spot checks (such as tracking 10 invoices per month throughout the entire supply chain)

FAQ

Will a digital signature be required for e-invoices in 2026? It is not mandatory in all cases, but in many situations it can provide strong evidentiary value and simplify the process. The decision depends on the delivery channel and process controls.

Is it sufficient to send the invoice as a PDF via email? A PDF sent via email alone is often insufficient if there is no auditable process in place (who sent it, when, what was the content, is it intact, how is it stored). By 2026, it will be advisable to reinforce this with controls or a structured channel.

What does “submission” mean in the context of e-invoicing? For most companies, it refers to data reporting via NAV Online Invoice. The goal here is not only submission, but also managing statuses, errors, retries, and supporting documentation.

How long must an e-invoice be retained? In Hungarian practice, this is typically several years; in many cases, the standard is eight years. The exact requirement may depend on the company’s specific circumstances and the type of document.

What should I look out for when switching to a new ERP or invoicing system? Make sure there is a migration plan for the archive and supporting documents (metadata, tax authority status, delivery confirmation), and conduct a sample audit after the migration.

What is the fastest way to reduce risk in 2026? Egy rövid gap-felmérés és 10-20 számlán végigvezetett end-to-end „trace” (kiállítás → NAV → kézbesítés → archívum), majd a hiányzó kontrollok célzott javítása.

Next step: Stabilizing e-invoice compliance and integration with Syneo

If you want to set up your e-invoicing process in 2026 in a way that stands up to an audit while also paving the way for automation (accounting, approval, ERP integration), it’s a good idea to start with a brief assessment.

The Syneo team typically provides assistance with the following aspects of e-invoicing projects:

Gap analysis of current processes and systems (exhibitions, NAV, archives)

NAV integration stabilization (statuses, retries, logging, monitoring)

Establishing archiving and access control procedures

Support for ERP/CRM/DMS integration planning and implementation

Contact and Additional Services: Syneo