Electronic Invoicing Regulations in 2026: A Brief Summary

E-Invoice

Electronic Invoicing Regulations 2026 — A Brief Summary | Syneo

2026 Overview of Key Legislation and Corporate Requirements for Electronic Invoicing: NAV Data Reporting, EN 16931, eIDAS, Archiving, and Access Management.

electronic invoice, e-invoicing, NAV, EN 16931, eIDAS, archiving, audit, digitization, compliance, Syneo

April 9, 2026

By 2026, electronic invoicing will no longer be a mere “convenience feature,” but rather a matter of compliance, integration, and operational stability for an increasing number of companies. The good news: most of the requirements aren’t complicated. The bad news: what is complicated is typically not the invoice PDF itself, but rather audit trails, reporting to the National Tax and Customs Administration (NAV), handling structured formats, and archiving.

This article provides a brief overview of the 2026 legislation, specifically from a corporate perspective (finance, IT, administration). It does not constitute legal or tax advice; in specific situations, it is advisable to consult with an expert.

What counts as an electronic invoice in 2026?

Under Hungarian and EU regulations, the essence of an e-invoice is not that it is an “invoice sent electronically,” but rather that the following are ensured throughout the invoice’s entire lifecycle:

the authenticity of the source (it can be verified who it comes from),

the integrity of the data (it has not been altered without detection),

readability (understandable to humans, capable of being presented during an audit).

This can be achieved in several ways (for example, through signatures, EDI, PEPPOL-type channels, or auditable internal controls). In corporate practice, the question in 2026 will be:

“Can I prove the origin, status, and authenticity of the invoice even in the event of a dispute or a tax audit?”

The main legal pillars that must be complied with by 2026

1) Hungarian regulations (VAT and accounting)

The legal framework for e-invoicing is typically provided by the following:

VAT Act ( issuance of invoices, data content, principles of authenticity, integrity, and legibility)

Accounting Act (documentation requirements, retention, auditability)

related implementing rules on invoicing, record-keeping, and auditing

Official reference source: the National Legislation Database.

2) NAV Online Invoice and Data Reporting Compliance

In Hungary, the "digital backbone" of invoicing has been the NAV Online Invoice data reporting system for years. By 2026, e-invoice compliance will effectively be divided into two parts for most companies:

Invoice generation and delivery to the partner (B2B/B2C/B2G channels)

Data reporting to the NAV (valid XML, proper status management, prompt correction of errors)

Initial information and login interface: NAV Online Invoice.

3) EU framework: eIDAS, EN 16931, and the digital VAT initiative

Two EU regions worth visiting in 2026:

eIDAS Regulation: the framework for electronic signatures and trust services (if you work with signatures and time stamps). Source: eIDAS (EUR-Lex)

EN 16931: the European e-invoice data model (particularly important for structured e-invoicing). Overview: EU e-invoicing building block

In addition, the "VAT in the Digital Age" (ViDA) initiative is underway at the EU level, which reinforces the shift toward digital reporting and e-invoicing. Overview: European Commission, ViDA

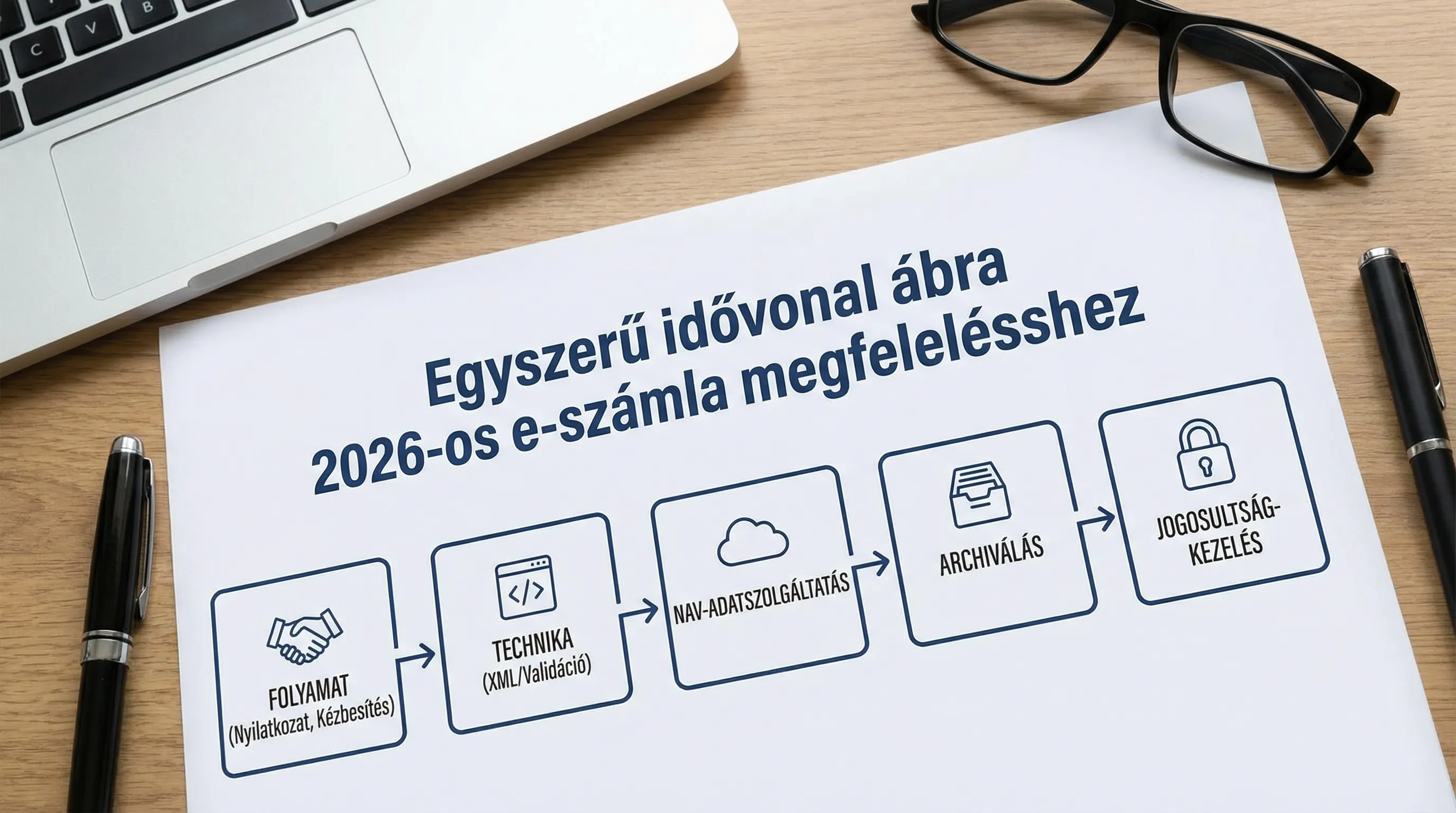

What does this mean in practice in 2026? (The 6 most important compliance topics)

1) Transmission and reception: it should be clear what constitutes an “accepted channel”

Many audit and dispute situations are not technical in nature, but rather related to processes:

who accepts e-invoices and how,

Through which channel is the delivery made,

what counts as “delivered” (proof of delivery),

where and how approval takes place.

If you don’t document this, your system may be technically sound, but it will be difficult to defend during an audit. In this regard, an auditable partner agreement or statement can be useful. (Syneo Background: E-invoice Statement: What Should It Include to Be Audit-Ready?)

2) Data content and master data quality: this is where most errors originate

By 2026, most of the typical e-invoice issues will not be “regulatory” but rather related to data quality:

errors in partner tax ID, address, and country code,

inconsistencies in product and service master data,

Mismatch between the VAT rate and the fulfillment logic,

Different rounding rules across systems.

These issues lead to NAV error codes, rejected invoices, and ultimately manual corrections. A practical approach to troubleshooting: NAV e-invoices: common errors and quick solutions for businesses

3) Structured e-invoices and EN 16931: On the IT side, this is a format and validation project

By 2026, it will become increasingly common for e-invoices to be not just “readable documents,” but structured, machine-processable data (such as XML-based data). This is important because:

accounting and invoice processing can be automated,

exception handling is reduced,

Validation and partner compliance can be standardized.

If your company integrates ERP, CRM, an online store, and logistics, structured e-invoicing quickly becomes a "system integration" issue. For technical details: Electronic invoice XML format: fields, validation, EN 16931

4) Digital signatures in 2026: not always mandatory, but sometimes a powerful risk mitigator

Frequently asked question: “Is a digital signature required for e-invoices?” The real answer is typically not black and white. In 2026, a viable approach for many organizations is that:

or you can verify the authenticity with a signature and a timestamp,

or you build a closed, auditable process and integration that is just as secure.

Decision-making considerations: Digital signatures on electronic invoices—will they be required in 2026?

5) Archiving and retrievability: “Having it” isn’t enough; you also have to prove it

Typical expectations for archiving in 2026:

the invoice must be searchable (by metadata, serial number, partner, or date),

the integrity must be verifiable (versioning, controlled storage),

can be produced quickly during an inspection,

access should be restricted (who can view it, who can export it).

For operational and corporate checklists: E-Invoice 2026: Checklist for Issuance and Archiving

6) Access control and logging: By 2026, this will be a minimum requirement for information security

E-invoicing involves the transfer of financial and tax data, so by 2026 it will be more than just a matter of “invoicing software.” At a minimum, it must include:

role-based access,

strong authentication (e.g., MFA, where appropriate),

Control of admin and integration access,

logging and regular review.

Practical Security Basics: E-Invoice Login: Access Management and Minimum Security Requirements

The 2026 "Minimum Compliance" Table from a Corporate Perspective

The table below provides a quick overview of what to ask about when it comes to finance, IT, and accounting.

Area | What does the company need to know in 2026? | Typical evidence / output |

Emissions | Standardized process, responsible parties, channels | Brief procedural guidelines, accountability matrix |

Admission | Accepted formats, error handling | Submission rules, approval workflow |

NAV Data Reporting | Stable integration, error handling, monitoring | Error statistics, logs, retry mechanisms |

Structured e-invoice (EN 16931) | Validation, field mapping, partner compatibility | Validation reports, test suite |

Archiving | Preservation, retrieval, integrity | Retention Policy, Access Logs |

Safety | Permissions, logging, controlled administration | RBAC list, audit log extract, audit report |

A brief, 30-day preparation plan for 2026

If you need to bring your e-invoicing system into compliance right now, the quickest way is usually not to purchase new equipment, but to conduct a brief assessment and make targeted improvements.

Week 1: Overview and Risks

Take a look:

Through which channels do you issue invoices and accept payments,

where the invoice is generated (ERP, invoicing software, online store),

Is there a documented statement or agreement with the partners,

What are the most common NAV errors, and how long does it take to fix them?

Week 2: Process and Responsibilities

This is where 70 percent of the results are usually determined:

who approves,

who fixes NAV errors,

What are the internal deadlines and SLAs?

What is the "source of truth" (sometimes the final invoice, sometimes the archive)?

Week 3: Technical stabilization (validation, logging, monitoring)

Goal: fewer manual corrections, faster triage. This typically includes:

XML validation prior to publication,

idempotent submission and retry/backoff,

logging in a way that allows it to be used in error tickets as well.

Week 4: Archiving and Audit Package

In the end, you should have an "audit package":

a brief description of the process,

access rights and responsible parties,

the process of archiving and retrieval,

Tracking 2–3 sample invoices (issuance, delivery, tax authority status, archiving).

For a more detailed implementation guide: How to Implement Electronic Invoicing: A Practical Guide for Beginners

Common Misconceptions in 2026

“If I send it as a PDF via email, it’s definitely not an e-invoice.”

That’s not necessarily true. The key factors are authenticity, integrity, readability, and a verifiable process. However, PDFs sent via email are often riskier from an audit trail perspective than a structured or controlled channel.

“Data reporting to the NAV replaces the submission of invoices.”

No. The data reporting submitted to the NAV and the invoice provided to the customer are not the same process. These two systems need to be synchronized.

“All IT has to do is set it up, and Finance just uses it.”

For e-invoicing to operate smoothly in 2026, a unified governance structure is needed (covering finance, accounting, IT, and often sales and logistics as well).

Frequently Asked Questions

Which laws should I consult if I switch to electronic invoicing in 2026? The starting point is typically the VAT Act and accounting regulations, supplemented by the NAV Online Invoice data reporting rules. At the EU level, eIDAS and EN 16931 are the most commonly cited standards.

Will structured (XML) e-invoicing be mandatory in 2026? In many cases, it is not presented as a “general requirement,” but rather as a partner expectation and a prerequisite for automation. However, by 2026, more and more business processes will be built around it, so it is advisable to prepare for it from a technical standpoint.

Will a digital signature be required for electronic invoices in 2026? Not in all cases. Signatures and timestamps are a strong means of demonstrating compliance, but in certain scenarios, auditable process controls, EDI, or integrated systems can also provide defensible compliance.

What is the most common mistake that makes an e-invoice appear to be a “regulatory issue” when it isn’t? Errors in master data and inconsistent data logic (tax ID, address, VAT treatment, rounding), which lead to NAV errors, rejected invoices, and manual corrections.

How can I quickly assess whether my e-invoicing process is audit-ready? Select 2–3 invoices and walk through the entire process: issuance, proof of delivery, tax authority statuses, archiving, and access. If you have to “search manually” for evidence at any point, that’s where the process needs improvement.

How can Syneo help with this?

If, by 2026, compliance with electronic invoicing regulations has become an integration and operational challenge for your organization (NAV errors, unreliable archiving, inconsistent processes, disputed invoices), then it’s worth considering not just a new tool, but a quick, targeted overhaul.

The Syneo team can provide support through IT and digital transformation consulting, for example:

in an assessment of the e-invoicing process and audit trail,

In stabilizing the NAV Online Invoice integration,

in the development of a validation and test package for structured e-invoices (EN 16931),

in setting minimum standards for archiving and access management,

Integrating ERP, accounting, and invoicing systems.

To proceed, check out the related materials (e.g., E-Invoicing 2026), or contact Syneo at syneo.hu to schedule a brief consultation.